The Myth of "Too Risky, Too Long, Too Expensive"

When I mention life science investing to angels, I often see the same reaction: a slight grimace followed by concerns about billion-dollar capital requirements and decades-long waits for returns. It's one of the most persistent myths in angel investing that life science companies represent a high-risk, low-reward proposition requiring endless patience and deep pockets.

The data tells a dramatically different story.

According to the Angel Capital Association's 2022 Angel Funders Report, life sciences now represent about one-third of all angel deals and have displaced longtime favorites like enterprise software. More importantly, healthcare and life sciences lead the pack with the highest median returns across all angel investment categories—with:

- Expected Return Multiples: Life science startups typically aim for exit multiples of 8x to 20x within five to seven years, although timelines can sometimes extend to ten years, depending on the segment. These high multiples reflect both the risk and potential upside inherent in the sector.

- Angel Investor Overall Returns: According to 2022 and 2023 data, the median internal rate of return (IRR) across sectors was 22%, with top quartile investments reaching 30–40% IRR. Portfolios that include multiple startups and diversify, especially into high-growth sectors like biotech and health tech, tend to perform better. The average return for early-stage rounds across all sectors is approximately 3.2x over 8–10 years.

- Life Science as a Focus Area: Health and life science startups account for about a third of all angel investment deals. Returns in these areas often rival, and at times exceed, traditional tech investments due to the large potential markets for successful products and the impact of scientific innovation.

- Top Performers: Some individual angels with a specialized focus on sectors including healthcare and biotech (e.g., Esther Dyson) have consistently achieved exit rates above 60%—meaning a strong proportion of their portfolio companies reach a profitable exit such as acquisition or IPO.

Understanding Different Risk Profiles

When evaluating investment opportunities, it's crucial to recognize that not all risk is created equal. The typical SaaS company faces minimal technology risk—most software can be built with enough time and talent. What SaaS companies do face is substantial market risk: will customers actually pay for and adopt the solution?

Life science companies present a fundamentally different risk profile:

- Science risk: Can the underlying biological hypothesis be proven?

- Regulatory risk: Will the innovation satisfy FDA requirements?

- Commercialization risk: Can the product reach its intended market effectively?

What many angels miss is that these risks can be systematically addressed and mitigated in ways that often make life science investments more predictable than their tech counterparts.

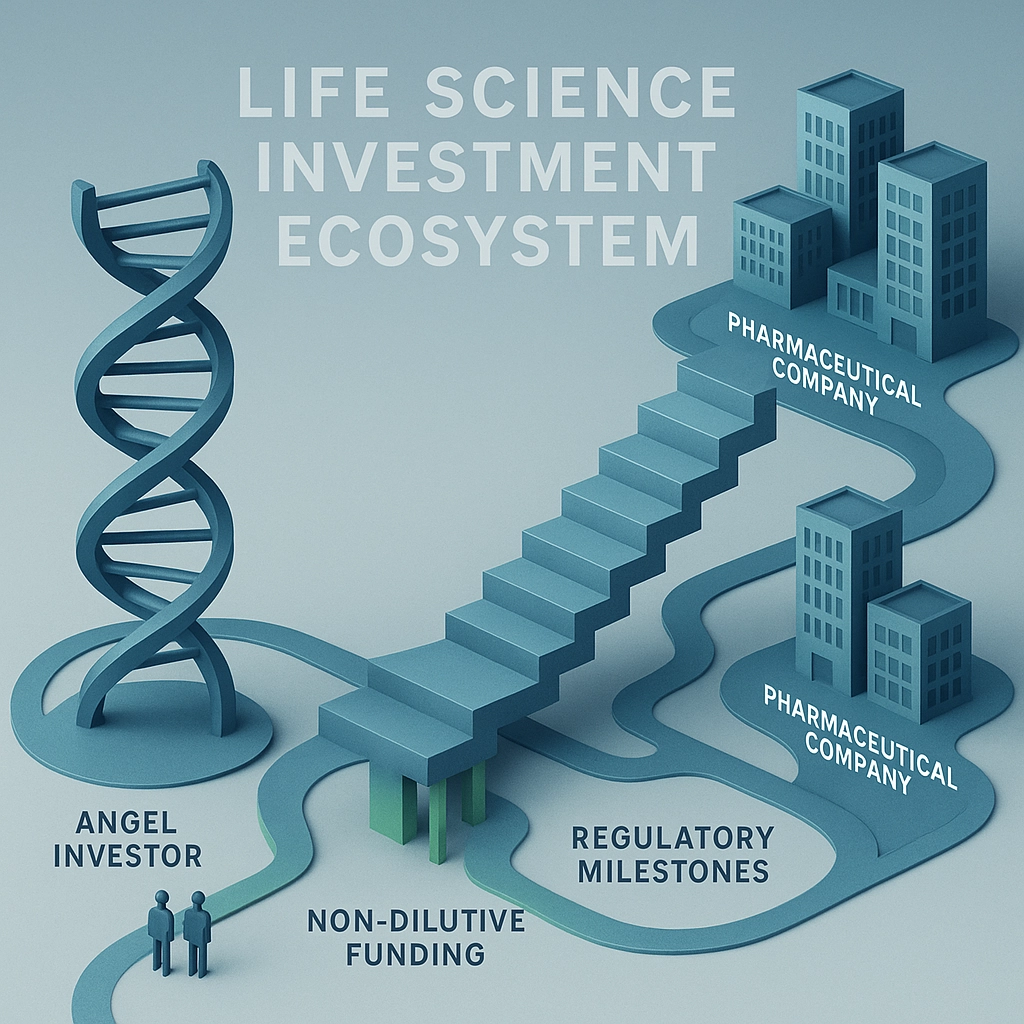

The Life Science Ecosystem: Built-In Risk Reduction

The life science sector has developed robust mechanisms for reducing investor risk:

- Non-dilutive funding: SBIR, NSF, and state-level grants (like Colorado OEDIT Advanced Industry grants) help companies prove their scientific hypotheses with government funds rather than investor capital.

- Staged development: The regulatory pathway provides clear, measurable milestones that create natural inflection points where value increases significantly.

- Industry acquisition appetite: Large pharmaceutical and medical device companies increasingly acquire innovations rather than developing them internally—leading to the mantra, "M&A is the new R&D."

The "Off-Ramp" Reality of Life Science Exits

Perhaps the biggest misconception is that life science investors must wait for full FDA approval and commercial launch to see returns. The data shows a completely different reality:

- 60-70% of successful exits in biotech happen before FDA approval (during preclinical, Phase I, II, or early Phase III), typically through acquisitions by larger pharma companies

- Only 20-30% of venture-backed drug development companies commercialize a drug themselves after FDA approval

- A smaller portion (10-15%) exit via IPO, often before approval

These statistics from BIO Industry Analysis, EvaluatePharma, and McKinsey reports on biotech M&A trends reveal that most value is realized pre-commercialization, at key inflection points like completion of IND (Investigational New Drug) applications, positive Phase II data, or special FDA designations.

Real Returns: Faster Than You Think

One of our best investments at Rockies Venture Club contradicts everything angels "know" about life science timelines. The company's financial model projected zero revenue for the first five years—a red flag in most sectors. But their explicit strategy was never to sell commercially. Instead, they planned to:

- Take our investment capital

- Complete FDA approval for their medical device

- Sell the company immediately after approval

The result? The company exited in just 18 months with an Internal Rate of Return (IRR) exceeding 150%. While not a 10X outcome, the compressed timeframe delivered nearly triple the annual returns we might see from a 10X exit over a longer period.

"M&A is the New R&D"

The life science landscape has fundamentally changed. R&D investments at large pharmaceutical and medical device companies continue to decline, while M&A activity remains robust. These industry giants increasingly prefer purchasing de-risked technology rather than building it themselves.

Decline or Adjustment in Big Pharma R&D?

- WSJ reported significant R&D cutbacks in 2024 by companies such as Pfizer, Bristol‑Myers Squibb, Bayer, and Novartis. These were driven by patent expirations and regulatory pressures, with clinical trial starts down ~22% from 2021 levels (Reference = Wall Street Journal)

- Return on R&D investments across the top 20 pharma companies dropped from ~6.8% in 2021 to just 1.2% in 2022 — a steep decline in productivity Drug Discovery Trends.

- Although funding rebounded afterward, 2024 marked a deeper decline in R&D deals between firms compared to prior peak years (Reference = Drug Store News)

Surge in M&A Activity

- Major uptick in early‑stage acquisitions: Q1 2025 saw biopharma M&A value surge by 101% compared to Q4 2024—from $18.8 bn to $37.7 bn (Reference = Pharmaceutical Technology)

- PwC’s mid‑2025 review reports pharma & life sciences M&A deal counts were resilient, with deal values declining slightly but still firmly in $1–5 bn bracket range and acquirers increasingly targeting earlier‑stage assets (Reference = PWC).

- IQVIA finds the share of commercial‑stage deals dropped sharply in 2024 to just ~8% of M&A value—while nearly half of deal value came from pre‑Phase III or earlier assets (Reference = IQVIA).

- Patent cliff dynamics are pushing Big Pharma to refill pipelines via acquisition rather than in‑house discovery alone (Reference = Financial Times).

This shift creates a tremendous opportunity for angel investors. By investing in companies at the earliest stages and supporting them through key value-creating milestones, angels can participate in exits that occur long before traditional commercialization—often at significant premiums.

The Four Faces of Life Science

It's important to recognize that "life science" encompasses several distinct categories with different risk profiles and investment timelines:

- Therapeutics/Drug Development: Highest regulatory hurdles but also highest potential returns

- Medical Devices: Often faster regulatory pathways with clearer technical requirements

- Diagnostics: Growing sector with multiple regulatory and reimbursement pathways

- Digital Health: Combines elements of traditional tech and healthcare, often with reduced regulatory burden

Each category requires specific due diligence approaches, but all can deliver strong returns when evaluated properly.

The State of Life Science Investing Today

The life science sector has never been more accessible to angel investors. Multiple factors create a favorable environment:

- Advances in technologies like CRISPR, AI-driven drug discovery, and precision medicine are accelerating development timelines

- The pandemic highlighted the strategic importance of robust biomedical infrastructure

- Non-dilutive funding sources have expanded

- Industry consolidation has created clear acquisition pathways for promising innovations

As one of the few sectors showing consistent growth regardless of broader economic conditions, life sciences represent both financial opportunity and potential for meaningful impact.

Practical Considerations for Angels

For angels considering life science investments, several strategies can help optimize returns while managing risk:

- Understand the exit strategy from day one: Is the company targeting acquisition after a specific milestone, or planning full commercialization?

- Evaluate non-dilutive funding potential: Strong grant funding can substantially extend runway without diluting early investors.

- Assess the competitive landscape: Understand where the company fits in the ecosystem and who potential acquirers might be.

- Consider syndication: Life science deals benefit from investor groups with complementary expertise in science, regulation, and commercialization.

- Look for multiple value inflection points: The best investments offer several potential exit opportunities at different stages.

Conclusion: A Category Worth Embracing

Far from being too risky, too long, or too expensive, life science investments represent one of the most attractive categories for angel investors. With built-in risk mitigation mechanisms, clear value inflection points, and strong acquisition markets, these companies can deliver superior returns compared to other sectors.

The data is clear: angels who systematically avoid life sciences are missing out on what has become the highest-returning sector in early-stage investing. By understanding the unique characteristics of these investments and applying appropriate due diligence frameworks, angels can participate in innovations that not only generate financial returns but also advance human health and wellbeing.

For angels looking to optimize their portfolios, the question shouldn't be whether to invest in life sciences, but rather how to develop the expertise needed to do it effectively.

Learn more about life science investing opportunities and strategies at our upcoming events or by contacting our team at Rockies Venture Club.

.jpg)

.jpg)