Startup dilution is a topic that makes even seasoned founders and investors wince. It evokes fears of lost ownership, reduced control, and blown-up cap tables. But here's the truth: dilution is not inherently bad. It’s the price of growth. What matters is how you plan for it, model it, and time it.

Over the past decade, dilution norms have changed significantly, and if you’re still using the “old rules” — like automatically raising for 18 months of runway or giving away 30% in your seed round — you may be setting yourself up for failure.

Let’s dig into how founders and investors can take a smarter approach to dilution that aligns with today’s venture landscape.

Timeless Advice: Model Your Capital Path to Exit

Before discussing market shifts, let’s revisit a principle that has never gone out of style:

Founders must model their capital raises with their exit in mind — not just survival.

That means identifying value inflection points (e.g., MVP launch, regulatory approval, first major customer, $1M ARR) and calculating the minimum capital required to reach each of those milestones. Then raise just enough to hit the next value inflection point — not to survive for 18–24 months arbitrarily.

Yes, many startups take 18–24 months between rounds, but that’s not the point. Investors don’t fund runway. They fund results. And if you fail to hit results, you’ll be lucky to raise another round at all — much less at a higher valuation.

The best time to raise is immediately after achieving a milestone, when your valuation jumps. That’s when you’ll take the least dilution per dollar raised.

At Rockies Venture Club (RVC), we use a simple yet powerful tool — a Capital Strategy Table — that helps founders model each round of funding, how much dilution they’ll incur, and what their exit ownership will look like. We also layer in our Cap Table Valuation Method, which accounts for cumulative dilution and employee option pools, providing a much clearer picture than most startup models.

Don’t Forget the Option Pool — It’s a Big Deal

One of the most overlooked sources of dilution is the employee option pool.

Many founders forget to model this into each round — or worse, they let investors structure it pre-money and don’t adjust the math afterward. This can result in a huge loss of founder ownership by the time of exit.

Most startups see 3%–10% dilution per round from option pool expansions or top-ups. By exit, that adds up to 18%–20% of the company. Failing to model this means your exit projections could be off by a fifth of the company’s value.

Founders and investors alike must make the option pool a first-class citizen in cap table planning. If you’re not modeling it, you’re not being realistic.

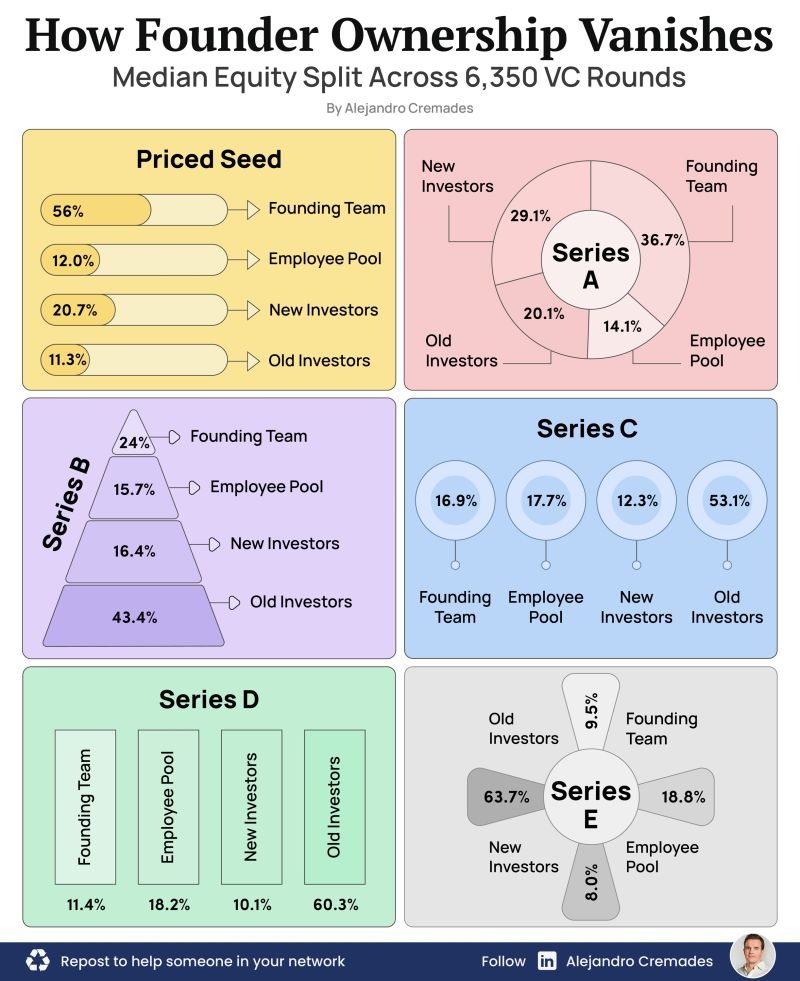

The New Norm: More Rounds Before Series A

Ten years ago, you might’ve raised a seed round and gone straight to Series A. Today? You might go through:

- Pre-seed

- Seed

- Seed II / Seed extension

- Bridge round

- Then Series A

Each of these raises chips away at ownership. If you’re not strategic about how much to raise and how much equity to sell at each step, you’ll find yourself without enough equity left to attract strong investors — or to reward yourself and your team for all the risk and work.

We’ve had companies offer RVC 49% of the company in a first raise — essentially Shark Tank territory. That’s not only a red flag for investors, it’s a cap table killer. Nobody wants to fund a startup where the founders are no longer motivated or where there’s no room left to bring in additional capital.

A good rule of thumb used to be “don’t give up more than 30% in any one round.” Today, that number is closer to 25%, and many top startups raise at 15%–20% dilution per round. That gives them enough fuel to grow while preserving equity for future rounds.

Beware of Mismatched Raise Sizes and Valuations

Here’s another common misstep: raising small amounts of money at sky-high valuations.

We’ve seen founders try to raise $500K–$1M at $10M or even $20M valuations. That’s only 5%–10% dilution, which may look good on paper, but in reality, it’s a trap.

With such a small raise, they can’t grow fast enough to “earn into” that valuation. When it’s time to raise again, they either:

- Fail to hit growth targets and get shut down by new investors

- Get squeezed into a down round or recap that wipes out early shareholders

- Lose credibility in the market because of unrealistic expectations

The goal isn’t to maximize valuation or minimize dilution. The goal is to raise enough capital to grow meaningfully — and do so at a valuation that reflects your current traction and projected progress.

A $2M raise at a $10M valuation (20% dilution) is often much healthier than a $500K raise at a $20M valuation (2.5% dilution) — because the former gives you a real shot at hitting milestones and setting up a stronger next round.

Focus on Exit Ownership, Not Just Pre-Money Valuations

At the end of the day, what really matters is how much you own at exit — not how high your last round’s valuation was.

Here’s a simple test: If your company sells for $100 million, what percentage will you actually own at that point?

The answer depends on:

- How many rounds you’ve raised

- The dilution you took at each round

- The size of the option pool

- Any convertible notes or SAFEs that stacked unconverted before priced rounds

- Whether there were down rounds, recaps, or liquidity preferences

It’s possible for a founder to raise a total of $10M and walk away with only 5% of a $100M exit — just $5M for all their years of effort. That’s not nothing, but it’s a far cry from the life-changing $20M–$30M they imagined when they started out.

That’s why we push all our founders to model cumulative dilution across multiple rounds, plan for a target exit size, and work backwards to determine raise sizes, round timing, and valuation targets.

Final Thoughts: Speed and Focus Beat Big Valuations

Many founders today are caught up in chasing large raises and high valuations — often encouraged by hype or fear of missing out. But the best strategy is still the oldest one:

Build real value, move quickly, raise strategically, and model your dilution carefully.

If you hit Product-Market Fit, raise enough to accelerate growth, not just survive. Don’t give away too much equity early, but don’t get greedy and hamstring your company’s future, either.

Dilution is not your enemy — poor planning is.

Whether you're a founder or an investor, taking the time to build a smart capital strategy is one of the highest ROI activities you can do.

.jpg)

.jpg)